Originally published in

The Business Times.

Date: March 11, 2026

Author: Madadh MacLaine

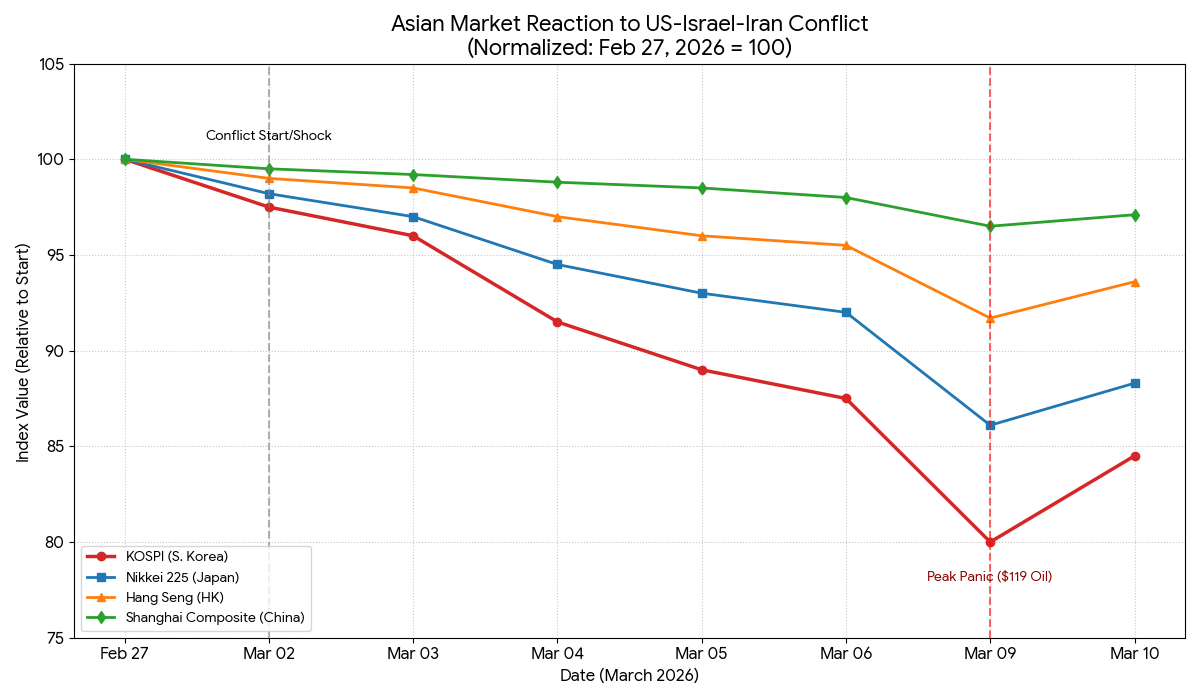

Asian markets breathed a collective, if shaky, sigh of relief yesterday. As of this morning, Brent crude has plummeted to $85.19 per barrel—a staggering $35 drop from yesterday’s peak of nearly $120 [ICE Futures/Trading Economics, 2026]. In response, the KOSPI has surged 5.4% and the Nikkei 225 is up 2.9%, clawing back ground lost during the peak of the Musaffah 2 crisis [Associated Press/Bernama, 2026].

But we must ask: For how long?

The smoke over the Strait of Hormuz today is more than a sign of regional conflict; it is the dying breath of an energy era that has held the Asia-Pacific hostage for a century. This morning’s market “recovery” is not a return to stability—it is a temporary reprieve granted by the whims of a 21-mile-wide waterway. For the Iron Triangle (Shipping, Energy, Finance), the lesson of the last 72 hours is visceral: Energy sovereignty cannot be found in a strait. It must be engineered through a Global Liquid Hydrogen (LH₂) Supply Chain.

The Fossil Fuel Trap: A Failed Status Quo

The volatility we are witnessing—where Brent swings 20% in a single trading session—is a systemic tax on Asian industrialism. Trump’s dismissive comments aboard Air Force One suggesting the conflict is “pretty much complete” may have calmed the algorithms, but they deliver a hard truth: the traditional “protector” of the sea lanes is no longer a guarantor of stability [CBS News/dpa, 2026].

While prices “plummet” back to $85, Singapore’s VLSFO bunker fuel remains stubbornly high at $1,110/MT, up nearly 50% from February lows [Bunker Index, 2026]. For the shipowner, the “blackmail” remains.

The Asia-Pacific Hydrogen Hedge

While the Strait remains a geopolitical trigger, the infrastructure to bypass it is “going live” in a multi-billion-dollar “green reality.” Asia is currently leading a strategic counter-strike to replace scarcity with technological abundance.

Who’s ahead in the Hydrogen Hedge?

APAC Hydrogen Readiness Index (2026)

| Country | Readiness Score (1–100) | Strategic Advantage | Current Vulnerability |

|---|---|---|---|

| China | 88 | 55% of global committed capacity; Inner Mongolian pipeline grid. | High total volume of crude imports. |

| Japan | 84 | World-first LH₂ carrier fleet (Kawasaki); $150B GX investment. | Extreme immediate dependency on Gulf LNG. |

| Australia | 81 | Murchison & Pilbara export hubs; “Renewable Quarry” status. | Domestic shipping fuel transition lag. |

| South Korea | 79 | World leader in fuel cell deployment; ₩187B clean ship fund. | High manufacturing energy intensity. |

| India | 62 | National Green Hydrogen Mission; $6B in active FIDs. | Severe reliance on Qatari LNG (30%). |

Industrial-Scale Execution (Australia & Korea)

This month, the Western Green Energy Hub in Australia secured major agreements to supply pure green hydrogen to Japanese and South Korean partners. The Lumsden Point expansion in the Pilbara is fast-tracking to feed renewable energy directly into Asian liquid hydrogen supply chains [Pilbara Ports/Marine Link, 2026]. Simultaneously, Hyundai Motor Group has announced a KRW 9 trillion ($6.3 billion) investment in the Saemangeum Hydrogen Hub, featuring a massive 200 MW PEM electrolyzer to ensure domestic energy self-sufficiency [The Investor/H2 Tech, 2026].

The Liquid Hydrogen (LH₂) Breakthrough

Past technical barriers are being crushed by “steel in the water” projects.. In January, Kawasaki Heavy Industries signed the contract for a 40,000-cubic-meter LH₂ carrier—thirty times the size of its predecessor, the Suiso Frontier [Hansa News, 2026]. This vessel is the maritime equivalent of the first supertanker, providing the foundation for a supply chain that ignores the Persian Gulf entirely.

Technical Challenges vs. Industry Solutions

There are still challenges ahead. Critics point to the “physics” of hydrogen as a barrier. The industry’s response? Engineering.

| Technical Challenge | Industry Solution & Real-World Example |

|---|---|

| Low Volumetric Density | Liquefaction Breakthrough: Chart Industries has reduced the energy penalty of cooling H2 to -253°C. Example: Samskip SeaShuttle (2027) uses deck-integrated cryogenic storage to maintain cargo space [Samskip/Chart, 2026]. |

| Wind Assisted Propulsion (WAP) | Reduces onboard power requirements by 10–30% with rotor sails and suction wings [IWSA, 2025]. |

| Boil-off Gas (BOG) | Active Reliquefaction: HD Hyundai developed the Hi-ERS system to re-condense gas during transit, ensuring zero fuel loss [KSOE/Lloyd’s Register, 2025/2026]. |

| Embrittlement | Metallurgy: IMO CCC 11 guidelines now mandate 316L austenitic stainless steel with >12% nickel to prevent lattice penetration [IMO Draft Guidelines, Sept 2025]. |

| Salt Sensitivity | Filtration: Toyota TME and Nedstack have deployed 2nd-gen PEM modules with hydrophobic membranes that block 99.9% of marine salt aerosols [Nedstack Technical Case Study]. |

| Infrastructure Gaps | • Green Shipping Corridors: Concentrating bunkering infrastructure on high-traffic routes to ensure reliable refueling before attempting a global rollout. Singapore, Rotterdam, and Los Angeles are building specific H2 bunkering terminals for 2027/2030 targets. • Shell “Holland Hydrogen I”: 200MW electrolyzer in Rotterdam to serve the major European shipping hub. |

Largest Hydrogen Projects

| Location | Capacity (GW) | Status |

|---|---|---|

| Australia | 70 GW | Environmental Approvals |

| USA (Texas) | 60 GW | Phase 1 (2 GW) Operational/Underway |

| China | 60 GW | 15th Five-Year Plan Integration |

| Kazakhstan | 40 GW | FEED Stage / FID Pending 2026 |

| South Africa | 40 GW | Strategic Planning (Long-term) |

| Mauritania | 30 GW | Feasibility / Framework Agreement |

| India | 30 GW | Development / Site Prep |

| Australia | 26 GW | EPC / Advanced Engineering |

| Oman | 25 GW | Land Allocated / Construction (Phase 1) |

| India | 20 GW | Under Construction |

Breaking the Blackmail: A Call to Action

- Asian Governments: Treat the IMO’s 2026 Net-Zero Framework (NZF) as a national security mandate. Implement “Marshall Plan” funding for hydrogen infrastructure and Contracts for Difference (CfDs) to bridge the price gap between volatile $90 oil and stable green hydrogen.

- Shipowners: Stop waiting for “the right time.” Every day a tanker sits idle in a conflict zone is a day that should have been spent commissioning a hydrogen-ready vessel, liquid hydrogen tanker, or a sail solution.

- Investors: Redirect CAPEX from fossil-fuel-dependent assets to the Japan-New Zealand Hydrogen Corridor and Australian export hubs [MOL/Marine Link, 2026].

Conclusion: Sovereignty is a Choice

The current “relief” in Asian markets is a dangerous illusion. If we remain tethered to the Strait of Hormuz, we remain tethered to the whims of regional instability and the shifting priorities of distant superpowers.

The success of Kawasaki, the ambition of Hyundai, and the resource wealth of Australia provide the blueprint. We can either stay tethered to a burning waterway or lead the transition to the hydrogen age. For the Asia-Pacific, energy sovereignty is not a climate goal—it is essential to surviving the 21st century.