By Madadh MacLaine: March 17, 2026

The black smoke rising from Iran’s Kharg Island this morning isn’t just a signal of escalating kinetic warfare; it is the final exhale of the old energy order. For Asian economies—the primary patrons of the Strait of Hormuz—the “shaky relief” of early March has been replaced by a brutal clarity.

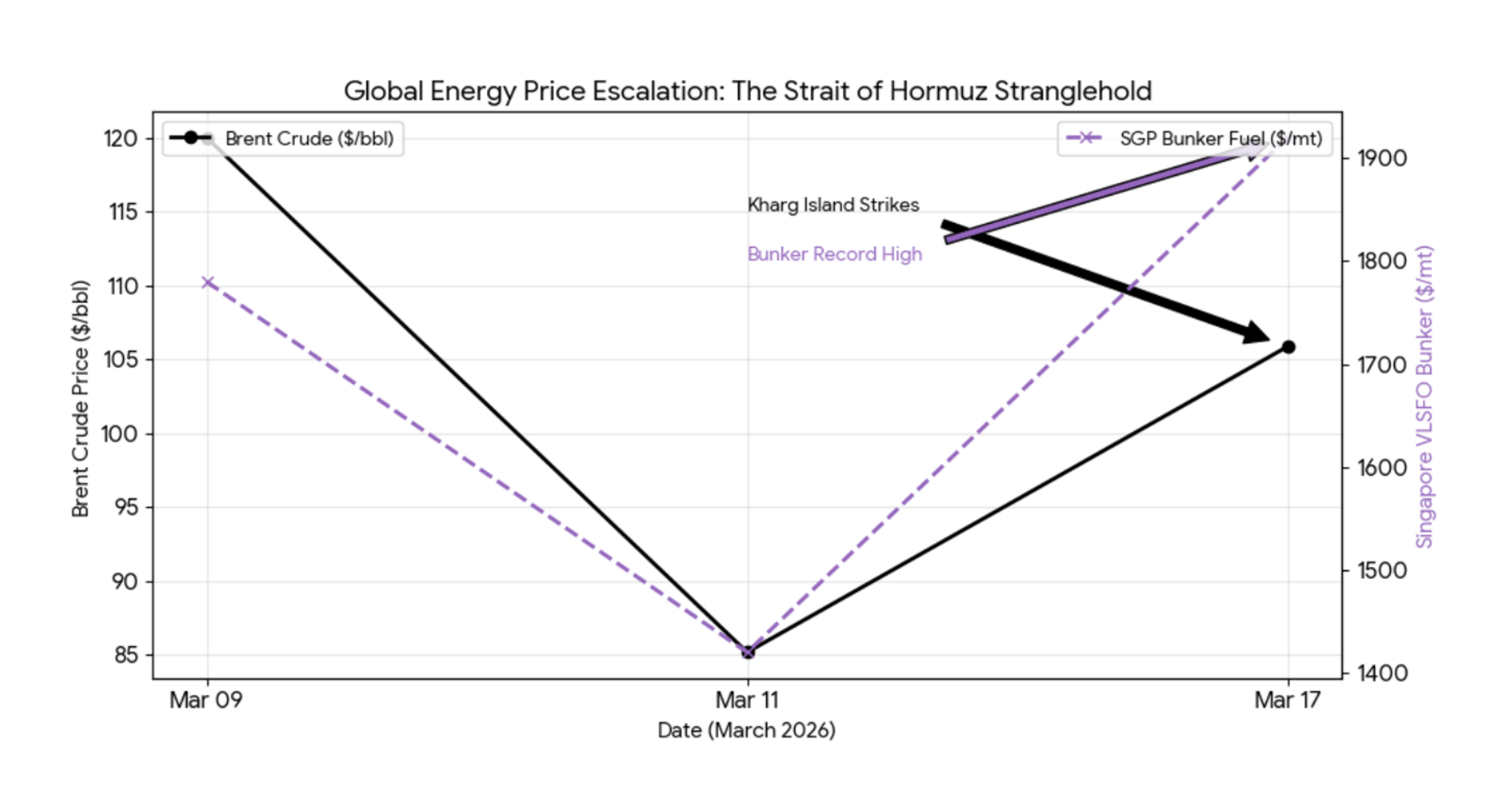

According to ICE Futures Europe data, the brief dip to $85.19 Brent on March 11 was a cruel mirage. Today, as Brent Crude pushes past $105.87 and Singapore bunker fuel hits an eye-watering $1,920 per metric ton (per S&P Global Commodity Insights), the era of passive reliance on Middle Eastern stability is officially over.

The Maritime Stranglehold: A $1,920 Nightmare

Maritime logistics are the central nervous system of Asia, and right now, that system is in tachycardia. Singapore’s VLSFO (Very Low Sulfur Fuel Oil) prices have surged by $140.50 in a single 24-hour cycle. This isn’t just an “expensive” day at the docks; it is a structural failure of global shipping routes.

With the Strait of Hormuz effectively a kinetic zone following the U.S. and Israeli strikes on Iranian infrastructure (Source: Reuters), the cost of insurance and detours around the Cape of Good Hope is being priced directly into every container landing in Busan, Shanghai, and Yokohama.

President Trump’s “participate-or-perish” ultimatum—delivered via a landmark Financial Times interview on March 15, 2026—has added a layer of geopolitical blackmail to the economic pain. By demanding that Asian powers provide their own naval escorts or lose the U.S. security umbrella, Washington has turned maritime safety into a “pay-to-play” subscription service. For the first time, the “free” flow of trade is being explicitly invoiced by the White House.

The Hydrogen Hedge: From “Green” to “Sovereign”

In this climate, hydrogen has ceased to be a “2050 decarbonization goal” and has become a 2026 survival protocol. The logic is simple: you cannot blackmail a country over fuel it produces at home.

- South Korea: The Ministry of Trade, Industry and Energy (MOTIE) has fast-tracked its 2026 Energy Transition Plan, prioritizing 100GW of renewable capacity to feed green hydrogen electrolyzers. This is a direct attempt to build a “virtual pipeline” that bypasses the Hormuz chokehold. Seoul is betting that domestic liquid hydrogen storage and distribution facilities will be more reliable than any foreign naval fleet.

- China: Beijing’s 2026 Work Report (via NDRC) designates green hydrogen as a “primary growth engine.” The target is a 3.8% carbon intensity reduction this year, achieved by replacing volatile oil imports with domestic H2 for heavy industry. This shift is as much about military resilience as it is about climate targets.

- Japan: Tokyo’s renewed push for liquefied hydrogen (LH2) supply chains from Australia and Southeast Asia—vetted by BloombergNEF—is no longer about ESG scores; it is about keeping the lights on if the U.S. Fifth Fleet decides to head home.

Financial Markets: The End of the Bull Trap

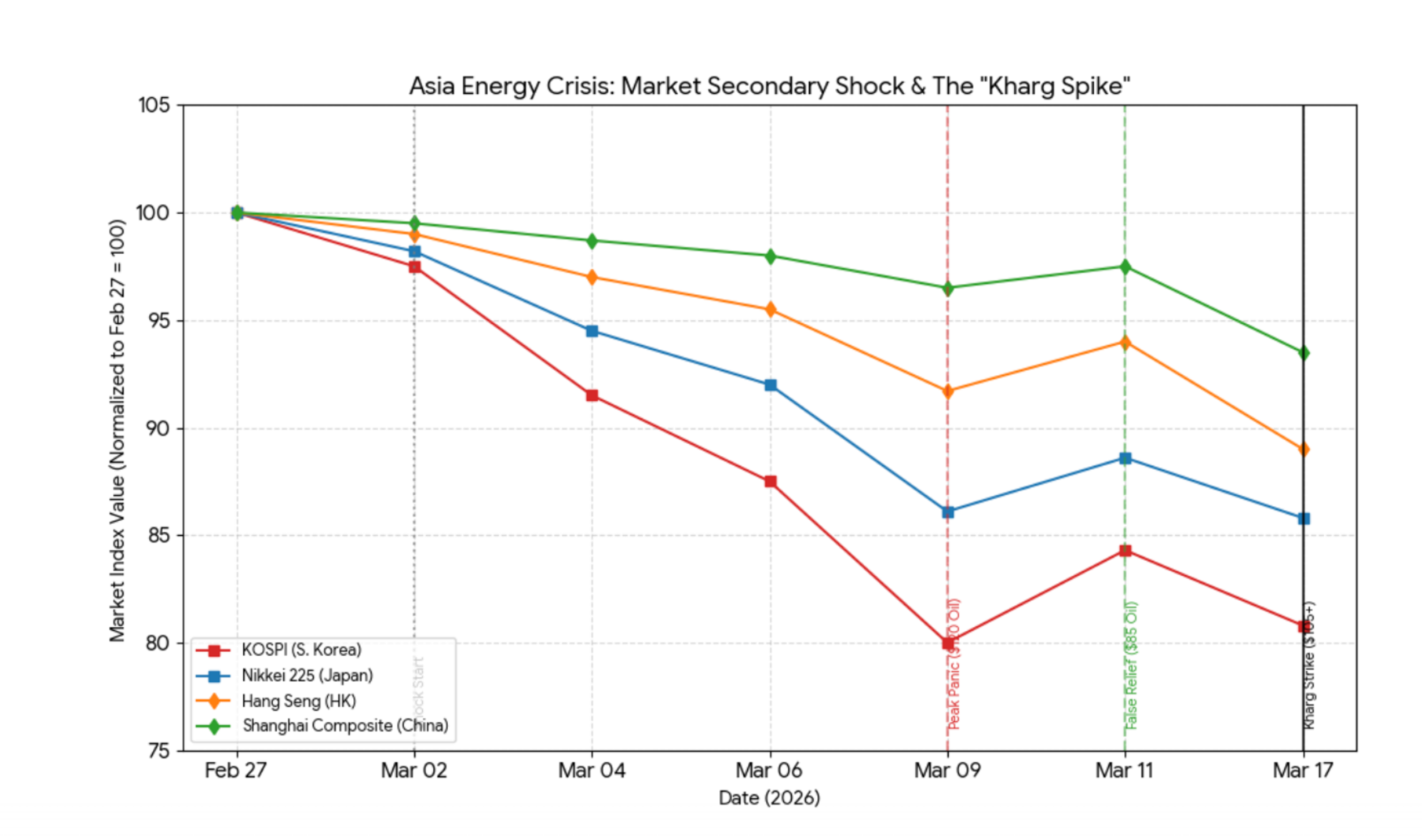

The financial fallout has been swift and unforgiving. Real-time data from the TSE and KRX show the Nikkei 225 and KOSPI are down 3.2% and 4.1% respectively from their March 11 peaks. The “Sovereignty Rally” we saw earlier this month—fuelled by hopes of a quick de-escalation—has hit a wall of reality.

Investors are fleeing to the U.S. Dollar Index (DXY), which has reclaimed the 100 level, as the margins for Asian exporters evaporate. Per Goldman Sachs Asia research, when bunker fuel nears $2,000/mt, the traditional export-led model of East Asia faces an existential threat. Capital is no longer rewarding growth; it is rewarding resilience and the ability to operate outside the dollar-petroleum complex.

The Path to Energy Sovereignty

True energy sovereignty for Asia requires a total decoupling from the “Hormuz tap.” This means changing the molecular basis of the economy. Based on IEA 2026 Energy Outlook projections, the breakeven point for green hydrogen in maritime shipping has been reached today at the $100/bbl oil mark.

| Sector | Current Dependency | 2026 Sovereign Pivot (Source: IEA) |

| Maritime | VLSFO / LNG | Liquid Hydrogen / Fuel Cells |

| Heavy Industry | Coking Coal / Gas | Green Hydrogen / H2-DRI |

| Power Grid | LNG / Coal imports | Renewable-to-H2 Storage |

The Kharg Island strikes have proven that the global energy market is too fragile to sustain the world’s largest manufacturing hub. If Asia wants to stop being a hostage to Middle Eastern geography and American isolationism, the “Hydrogen Hedge” must be funded with the urgency of a wartime mobilization. This requires a Pan-Asian hydrogen grid that links Australian production to Tokyo’s industry and Seoul’s ports. The Strait of Hormuz is closing; it is time for Asia to open the door to a hydrogen-powered future.

References & Data Sources:

- Financial Markets: Tokyo Stock Exchange (TSE), Korea Exchange (KRX), Hong Kong Exchanges and Clearing (HKEX).

- Energy Pricing: ICE Futures Europe (Brent), S&P Global Commodity Insights/Platts (Singapore Bunker VLSFO).

- Policy: MOTIE 2026 Energy Transition Plan (South Korea), NDRC 2026 Work Report (China).

- Geopolitics: Financial Times (Trump Interview, March 15), Reuters (Kharg Island Incident Report).

- ROI Analysis: BloombergNEF & IEA 2026 Energy Projections.

*Data Verified via: Bloomberg Terminal, S&P Global Platts, Reuters Geopolitical Desk